What is the key difference between FIFO & LIFO and the weighted Average Method?

FIFO method

An asset distribution strategy is known as First in, first-out or FIFO, in which the actual issue or selling of products from the stores is made from the oldest lot on hand. This follows a chronological order, i.e. this first disposes of the object which is first inserted into the inventory.

Therefore, this inventory valuation approach is the most suitable and rational. And most business people used to keep their inventory. Unless the products are perishable, they will quickly become redundant, so it will be better to first treat the earliest stock that minimizes the chance of becoming it outdated.

The remaining stock in hand would therefore eventually reveal the new stock at the current market price. The approach is the most suitable one when there is a decline in prices as the cost to produce would be greater than the cost to substitute.

However, if the prices are high, the same situation will be reversed and as a result, ordering the same quantity of materials without adequate funds is not easy.

LIFO method

LIFO or Last in, first out, is a valuation form of inventory accounting. This strategy is based on the premise that first the last item in the inventory will be sold out, i.e. organized alphabetically order will be followed when inventory is released from the shops.

The value of the unsold stock will be small as the economy inflates, while the value of the cost of the products sold will be high, which will eventually lead to low profit and income tax there too. While the whole situation will be reversed under deflationary conditions due to a decline in the general price level, resulting in higher revenues and taxes on wages.

While the statement is shown to be illogical and inconsistent with product movement within the company organization. To this end, the LIFO method is no longer adopted for inventory valuation.

Weighted Average

The weighted average process, which is used mainly to assign the average cost of output to a given commodity, is most frequently used when stock products are so interconnected that it is impossible to allocate a particular cost to a specific unit.

This is also the case when the respective product pieces are like each other. This approach assumes a store is selling all its inventories at the same time. This estimate yields the weighted average cost per unit — a number that can then be used to assign a cost to both the termination of the inventory and the sale

FIFO vs LIFO

LIFO Vs FIFO is a type of inventory management in which the last obtained product or item is used first and thus the inventory in hand consists of the earliest delivery.

On the other hand, FIFO is another form of inventory management in which the first obtained item is used first, i.e. the issue of products is made from the earliest lot, and the product in hand is made up of the last lot.

Inventory management is a difficult job for entirely stock-oriented organizations. Most techniques are used in inventory management. LIFO, FIFO, Simple Average, Base Stock, and Weighted Average, etc. are the approaches.

As you can see, FIFO vs LIFO has many variations. Now let us take a closer look at the key disparity between FIFO and LIFO:

- First in First out is the approach that most companies use. On the other hand, last in First out are few companies where the oldest products are kept in stock.

- First in First out, there are fewer layers of inventory to monitor and also reduce record keeping. Last in First out have comparatively more inventory layers to monitor which enhances record keeping.

- The profit and income tax are larger at first in First out. Last in First out is used to delay earnings tax payments.

- First in First out means the stock that was first introduced would be withdrawn from stock first. On the other hand, last in First out indicates inventory that was last introduced to the stock will be erased first.

- Usually, much higher preference is given to the First in First Out. Next in First out, the balance sheet gets a much lower priority.

FIFO and LIFO calculator

Online calculators are plenty if you do not want to get into the manual heavy calculation.

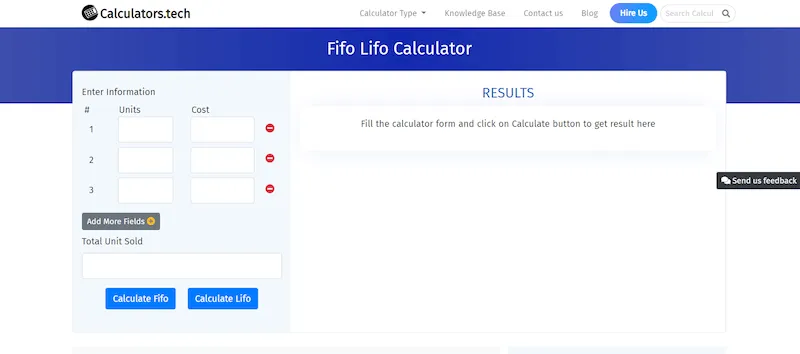

Calculators.tech

One of good and reliable FIFO calculator and LIFO calculator is Calculators.tech. it saves them time and energy of the users and they can calculate in abundance.

How does a calculators.tech work?

The method is very convenient and does not require much of a work. Inputs need to enter with the number of units along with the cost of each unit. P and S can be selected for each inventory by seeing the drop-down menu. There is an option of selecting between the FIFO calculator and the LIFO calculator. You can click on the calculator of your choice.

This is not desktop software that you have to download. It is free of cost web-based program. Anyone can get their hands on this tool.

Calculators online.net

Another exceptionally well-performed online calculator is calculator online.net. The experts behind this development claim it to be the best tool for the job. It works fine for calculating the inventory cost through the FIFO method. Similarly, last in first out technique is also used by this calculator which is called the LIFO calculator.

Just add the number of purchased products. After that enter the unit of each quantity with the price.

Lastly, add total units and click the button saying FIFO.

The same process is performed for LIFO calculations.

Conclusion

The difference between the weighted average, LIFO method, and FIFO method has been explained with clarity. Both methods have some pros and some cons. The good news is that the calculation of both methods has become easy. The tools that are being inverted has made life easier. One such tool is these FIFO calculators and LIFO calculator which are easily accessible online.

Comments